How to Read a Cash Flow Statement: A Beginner's Guide to Understanding Cash Flow in Business

Understanding financial statements is a crucial skill for anyone involved in business—whether you're an entrepreneur, investor, or manager. Among these statements, the cash flow statement is particularly vital because it provides insight into how money moves through a company. Unlike the balance sheet or income statement, which may show profitability, the cash flow statement shows actual cash inflow and outflow over a period of time.

In this comprehensive guide, we’ll break down how to read a cash flow statement and what each section reveals about a company’s financial health. By the end, you’ll be able to confidently analyze a cash flow statement to understand how a business generates and uses its cash resources.

What Is a Cash Flow Statement?

A cash flow statement summarizes the cash that flows into and out of a company over a specific period, typically monthly, quarterly, or annually. It is one of the three main financial statements that every business prepares, alongside the income statement and the balance sheet.

Unlike the income statement, which includes non-cash items like depreciation and accruals, the cash flow statement focuses strictly on actual cash transactions. This makes it especially valuable for assessing a company’s liquidity—its ability to cover short-term obligations and fund day-to-day operations.

The Three Main Sections of a Cash Flow Statement

A cash flow statement is divided into three sections:

- Operating Activities

- Investing Activities

- Financing Activities

Each section provides a different perspective on the sources and uses of cash within the business. Let’s break down each of these sections in detail.

Join the MB&A CPAs Community:

Stay connected with MB&A CPAs on social media through linkedin, facebook, instagram, twitter, tiktok, and youtube for the latest updates on industry trends, financial insights, and upcoming events.

Together, we can build a brighter future with accurate and insightful information.

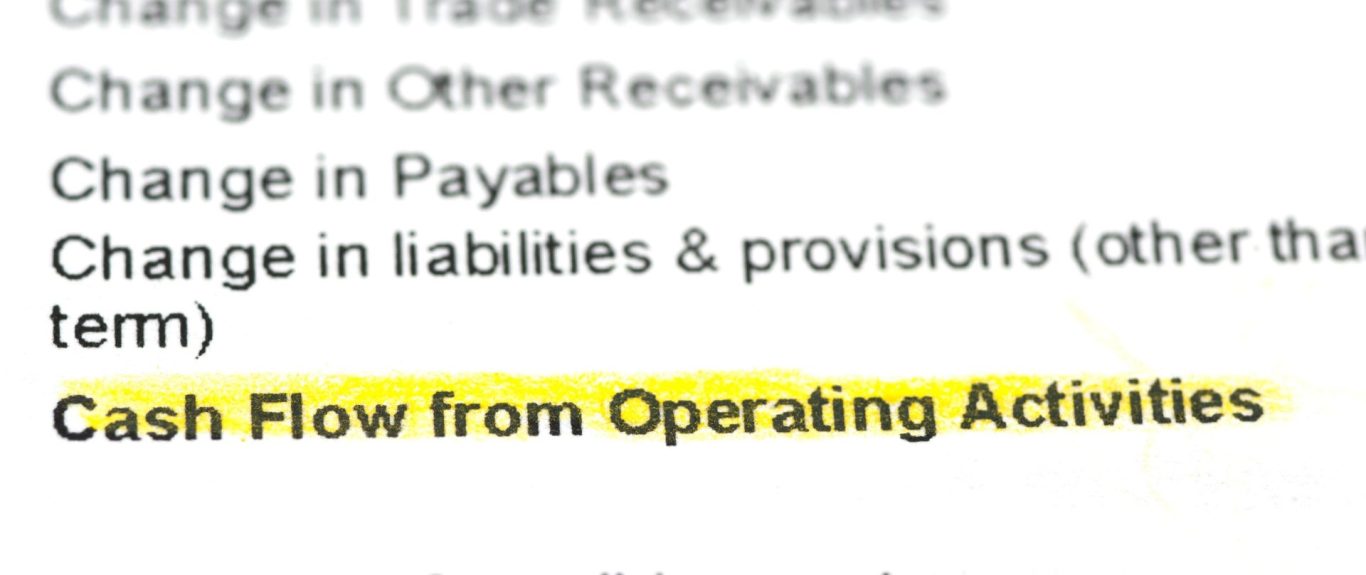

1. Operating Activities

The operating activities section of the cash flow statement reflects the cash generated or used by a company’s core business operations. This section helps you understand whether a business can generate enough cash from its operations to maintain or grow its operations without relying on external financing.

Key Items in Operating Activities:

- Net income: The starting point of this section is typically the company’s net income (from the income statement). However, since net income includes non-cash items (like depreciation or changes in working capital), these need to be adjusted.

- Depreciation and amortization: These are non-cash expenses deducted from net income on the income statement, but since they don’t affect cash, they are added back in the cash flow statement.

- Changes in working capital: Changes in current assets and liabilities—such as accounts receivable, inventory, accounts payable—are adjusted here. An increase in working capital (like higher accounts receivable) can indicate that cash is tied up in the business, while a decrease can signal cash is being freed up.

- Other operating cash inflows/outflows: For example, interest received, taxes paid, or other operational inflows and outflows that affect cash flow.

2. Investing Activities

The investing activities section details cash flows related to the purchase or sale of long-term assets, such as property, equipment, or investments. This section shows how much money the company is spending to acquire new assets or generating by selling existing ones.

Key Items in Investing Activities:

- Capital expenditures (CapEx): This represents the purchase of physical, long-term assets like property, plants, or equipment. CapEx typically involves a cash outflow and is subtracted from the operating cash flow.

- Proceeds from asset sales: Any cash inflows from the sale of property, equipment, or investments are recorded here.

- Investment in securities or acquisitions: Cash used for investing in stocks, bonds, or other companies is also included in this section.

Why It’s Important:

This section helps you assess whether a company is investing in its future growth by acquiring new assets, or if it’s divesting to focus on other areas. Negative cash flow from investing activities is not necessarily bad, as it might indicate the company is making valuable investments, but sustained negative cash flow can also signal financial distress if not matched with adequate funding from other activities.

3. Financing Activities

The financing activities section of the cash flow statement reveals how the company raises capital and repays investors and creditors. It includes cash inflows from issuing stock, debt issuance, or cash outflows from repaying loans, paying dividends, or repurchasing shares.

Key Items in Financing Activities:

- Issuance of debt or equity: When a company raises capital by issuing bonds, borrowing money, or selling stock, the cash inflow is recorded here.

- Repayment of debt: Payments on loans or bonds, including interest, are recorded as cash outflows.

- Dividends paid: Cash dividends paid to shareholders are recorded as an outflow in this section.

- Share repurchase: Cash used to buy back the company’s own stock also appears in this section.

Why It’s Important:

This section helps investors and analysts understand how the company is financing its operations and whether it is relying on debt, equity, or internal cash generation. A company that consistently borrows to finance operations might be taking on too much risk, while a company that consistently raises capital through equity issuance may be diluting its shareholders.

How to Read and Analyze a Cash Flow Statement

The cash flow statement shows how a company generates and uses cash over a period.

- The statement is divided into three sections: operating activities, investing activities, and financing activities.

- Positive operating cash flow is essential for long-term sustainability, while negative cash flow could indicate trouble.

- Look at investing and financing activities to understand how the company is funding its growth or managing its liabilities.

- The net change in cash at the end of the statement shows whether a company is growing its cash reserves or depleting them.

By mastering how to read a cash flow statement, you gain a clearer view of a company’s financial health and its ability to sustain operations, fund growth, and generate value for investors. Whether you’re looking at it for investment purposes, business decisions, or simply to understand your own company’s cash dynamics, it’s a powerful tool for financial analysis.

Now that you understand the basic structure, here’s how to read a cash flow statement and interpret its meaning.

Step 1: Look at Operating Cash Flow

Start by looking at the operating cash flow (also called cash from operations) to determine if the company is generating sufficient cash to fund its day-to-day operations. Ideally, you want to see positive operating cash flow, which indicates that the business is profitable at a cash level and doesn’t need to rely on outside financing.

Positive operating cash flow: The company can generate enough cash from its operations to meet obligations, pay dividends, and reinvest in the business.

Negative operating cash flow: This could signal that the company is not generating enough cash to cover its expenses, which might lead to financial trouble unless it can raise cash from financing or investing activities.

Step 2: Examine Investing Activities

Review the investing activities section to see where the company is putting its money. A company that is heavily investing in property, plant, and equipment (CapEx) may be in a growth phase, while a company selling assets might be trying to raise cash or divest non-core operations.

High CapEx: A sign that the company is investing in growth, but it could also put a strain on cash if not offset by operating cash flow.

Net cash inflows from investing activities: If a company is selling assets to raise cash, this might indicate that it’s struggling to fund operations through normal means.

Step 3: Assess Financing Activities

Finally, look at the financing activities section. A company might rely heavily on debt to fund operations, or it might raise capital by issuing equity.

Debt issuance: If a company is borrowing a lot, it might be funding growth or covering a cash shortfall. However, increasing debt could also be a red flag if the company is struggling to generate cash from operations.

Dividend payments: A company paying consistent dividends is often seen as financially stable, but if it’s paying dividends while having negative operating cash flow, it might be a sign of financial strain.

Step 4: Analyze the Net Change in Cash

At the end of the statement, you’ll find the net change in cash, which sums up the cash flow from all three sections (operating, investing, and financing). This tells you whether the company’s cash position has increased or decreased over the period.

Related Contents

")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

© Copyright. All rights reserved.

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.